The time period book worth is derived from the accounting follow of recording asset worth based mostly upon the unique historical cost within the books. Book worth can refer to a number of totally different financial figures while carrying value is utilized in business accounting and is often differentiated from market value. In most contexts, guide value and carrying worth describe the identical accounting concepts. In these instances, their difference lies primarily throughout the forms of firms that use each. Because the fair value of an asset may be more risky than its carrying value or e-book value, it’s potential for large discrepancies to happen between the 2 measures.

First the account takes the value of the item when it was first bought and recorded. The original cost of the asset — similar to software, equipment or trucks — is an effective starting place, however it doesn’t mirror an correct present worth. The asset has depreciated over time, slowly losing worth because of age and wear. To create the carrying worth, the accountant combines the original price of the asset with the depreciation cost (carried over from a separate account).

All three of these amounts are proven on the business stability sheet, for all depreciated property. A firm’s e-book worth is the amount of money shareholders would obtain if assets have been liquidated and liabilities paid off.

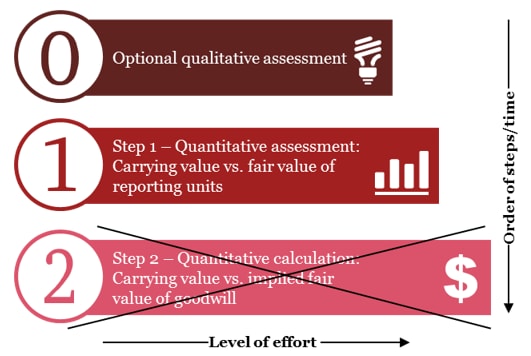

IAS 36 Impairment of Assets seeks to ensure that an entity’s property usually are not carried at more than their recoverable quantity (i.e. the higher of truthful worth less costs of disposal and worth in use). To calculate goodwill, the honest value of the belongings and liabilities of the acquired enterprise is added to the honest value of enterprise’ property and liabilities. The extra of price over the truthful worth of internet identifiable property known as goodwill. Goodwill is an intangible asset that arises when a enterprise is acquired by one other.

FINANCE YOUR BUSINESS

Consider the 2008 housing crisis when the market demand for mortgage-backed securities collapsed. Companies holding mortgage-backed securities as Level 1 assets noticed those property deteriorate to Level three belongings virtually in a single day. In consequence, most of the nation’s largest monetary institutions https://cryptolisting.org/ had to take huge asset write-downs (reductions in value) to adjust to SFAS 157. In flip, this lowered stockholder fairness in many monetary institutions as a result of owners’ fairness equals belongings minus liabilities.

Fair worth is an inexpensive and unbiased estimate of the intrinsic worth of an asset. Essentially, the truthful value of an asset relies on several factors such as utility, related prices, and supply and demand considerations. Another widespread definition of honest worth is the value that would be obtained for the sale of an asset or paid to switch a legal responsibility in a transaction between the market individuals at the measurement date.

It is essential to have knowledgeable equipment and tools specialist – someone who understands the many factors affecting the honest worth – carry out the valuation of the assets. A professional valuation specialist will calculate the fair worth of an asset, ensuring that an correct illustration of the asset has been considered and applied in the final conclusion of fair value. Appraisers contemplate the earnings, price, and market approaches to worth when performing a valuation. Fair value accounting requires companies to adjust property in a well timed method to replicate present market prices. This adjustment, known as “mark-to-market,” can typically hurt corporations in risky industries.

Fair value is an unbiased assessment of the value of an asset, good or service. Fair worth estimates permit for the approximate value of assets to be identified for functions of accounting, document preserving and sales negotiations. Fair value is a useful tool for understanding the financial standing of an organization. Market value is the present price the asset or firm could be offered for on the open market. Ideally, this is identical as the carrying and guide value, but this isn’t at all times true.

If multiple market is available, the “most advantageous market” must be used. Both the worth and costs to do the transaction have to be thought-about in figuring out which market is essentially the most advantageous market. Relying solely on the historic worth of belongings would not enable for other exterior factor, similar to modifications available in the market. With honest worth, you can estimate the adjustments to value for the reason that final estimation or set a fair price if no prior price exists. The more accurate the financial assessment of the asset is, the more informed any selections associated to the asset might be.

BUSINESS OPERATIONS

Book worth is the term which implies the value of the agency as per the books of the corporate. It is the value at which the property are valued in the balance sheet of the corporate as on the given date. In the futures market, honest worth is the equilibrium worth for a futures contract. This is the same as the spot worth after taking into account compounded curiosity (and dividends misplaced because the investor owns the futures contract somewhat than the bodily stocks) over a certain time frame. On the other facet of the steadiness sheet the honest worth of a liability is the quantity at which that liability might be incurred or settled in a present transaction.

What Is the Tax Impact of Calculating Depreciation?

The funding in XYZ Corporation is reported at value in the asset section of the stability sheet. In accounting, truthful value is used as an approximation of the market value of an asset (or liability) for which a market worth cannot be determined (normally because there isn’t a established marketplace for the asset). When an lively market does not exist different strategies have for use to estimate the fair worth. Assumptions used to estimate fair value ought to be from the angle of an unrelated market participant. This necessitates identification of the market by which the asset or liability trades.

- SFAS 157 has the target of eradicating uncertainty that asset stated values symbolize “honest value” in keeping with Generally Accepted Accounting Principles, or GAAP.

- Neither market value nor book value is an unbiased estimate of a corporation’s worth.

- However, relying on the type of asset, the market method or a mixture of the market and cost strategy could be more relevant in figuring out the fair value of the asset.

- If multiple market is available, Topic 820 requires using the “most advantageous market”.

- Fair worth is a useful gizmo for understanding the monetary standing of a company.

- Compare truthful market worth to honest value, which takes under consideration some grass root details a few specific purchaser or vendor.

Book worth also referred to as carrying worth or internet asset value Net Asset Value Net asset worth NAV is defined as the worth of a fund’s asseta minus the worth of its liabilities. The time period “internet asset worth” is usually utilized in relation to mutual funds and is used to find out the worth of the belongings held. Whereas the calculation of web book worth is an accounting perform, this does not present a true representation of the fair value of an asset. Conclusion The delivery van is a simplified example for example the differences between NBV and fair value. A company’s e-book worth is utilized in fundamental monetary analysis to assist determine whether the market value of corporate shares is above or below the book worth of corporate shares.

The market worth could be greater or decrease than the carrying worth at any time. These variations often aren’t examined until belongings are appraised or sold to help decide if they’re undervalued or overvalued. The following is an instance of tips on how to report investments of lower than 20% of shares — assume ABC Corporation purchases 10% of XYZ’s Corporation’s widespread stock, or 50,000 shares. When buying less than 20% of a company’s stock, the cost technique is used to account for the investment. ABC data a journal entry for the purchase by debiting Investment in XYZ Corp. for USD 50,000 and crediting Cash for USD 50,000.

Book value is an accounting merchandise and is topic to adjustments e.g. depreciation which will not be easy to understand and the company has been depreciating its belongings, one may have to. It is essential to understand that the book value is not the same as the fair market worth because of the accountants’ historical cost precept and matching precept. Book worth is the net assets value of the corporate and is calculated because the sum of whole property. Book value is often used interchangeably with “internet e-book worth” or “carrying value,” which is the unique acquisition cost less amassed depreciation, depletion or amortization.

Relevance of Fair Value Accounting to Consumers

MACRS lives are designed to recapture the price of belongings used in the operation of a business at an accelerated tempo. This increases money circulate and, in consequence, offers opportunities to reinvest the extra money circulate. Straight line basis is an easy approach to calculate the lack of an asset’s worth over time. This calculation is particularly helpful for bodily belongings—such as a chunk of kit—that an organization would possibly promote in whole or in parts at the end of its helpful life. Therefore, the e-book value of the 3D printing machine after 15 years is $5,000, or $50,000 – ($3,000 x 15).

The hole between the acquisition price and the e-book value of a business is known as goodwill. Accounting for goodwill is essential https://cryptolisting.org/blog/how-can-a-company-have-a-profit-but-not-have-cash to maintain the mother or father firm’s books balanced.

There might be no other changes aside from potential future impairment (and remember to adjust future depreciation expense – it is going to be lower since the asset cost is now decrease). Basically, any activity that occurs above its original value goes to OCI and any exercise that occurs beneath its original price goes to internet income. The guide value of an organization is important for accounting functions, and it’s a part of the review of the business if the enterprise is to be offered. Since guide worth isn’t related to the market worth of an individual asset, it can be used as a reference level, however not as a promoting value. The calculation of guide value for an asset is the unique price of the asset minus the accumulated depreciation to the date of the report.

The carrying value, or e-book worth, of an merchandise is said to business accounting. Accountants record the value of things primarily based on a variety bookkeeping of elements, including how much was spent for the merchandise, when it was first bought and how lengthy the merchandise has been used.

The supply van is a simplified example for example the differences between NBV and honest worth. One should contemplate that, for an asset-intensive enterprise Bookkeeping, the variations could be more severe, exhibiting a significant difference between NBV and truthful worth.

MARKET RESEARCH

In other words, the honest worth of an asset is the amount paid in a transaction between members if it’s sold in the open market. Due to the altering nature of open markets, nonetheless, the fair worth of an asset can fluctuate tremendously over time. Under US GAAP (FAS 157), honest value is the quantity at which the asset could be purchased or bought in a current transaction between willing parties or transferred to an equivalent party other than in a liquidation sale.

Neither market worth nor guide worth is an unbiased estimate of a company’s value. The company’s bookkeeping or accounting data don’t typically replicate the market worth of property and liabilities, and the market or commerce value of the company’s inventory is topic to variations. Monthly or annual depreciation, amortization and depletion are used to cut back the e-book value of belongings over time as they are “consumed” or used up within the strategy of acquiring revenue. These non-cash expenses are recorded in the accounting books after a trial steadiness is calculated to ensure that cash transactions have been recorded precisely. Depreciation is used to report the declining value of buildings and tools over time.

Amortization is used to document the declining value of intangible property corresponding to patents. In tax accounting, NBV calculates the annual depreciation of the assets with the aim of decreasing the taxpayer’s tax liability. Once the traditional useful lifetime of the asset has been absolutely depreciated, the NBV goes to zero and, as a result, there is no longer a tax benefit to the taxpayer. In the case of tax accounting, Modified Accelerated Cost Recovery System (“MACRS”) lives, that are published by the IRS, are usually used.

Book worth is equal to market value

As for reversals, I imagine under GAAP, you possibly can never write up mounted belongings, even when it is the recovery of a earlier How is materiality determined? impairment. So it’s extremely straight-forward; merely test for impairment, if it exists, write the asset down and e-book the loss.

Advertise Here